👋🏼 Hello friends,

Greetings from Saratoga Springs, NY! Let's take it easy and enjoy a leisurely Sunday Drive around the internet.

The Sunday Drive is also published at NewLanternCapital.com.

🎶 Vibin'

As you’ll see below, this week we’re talking about banking, money, and the price of money, i.e. interest rates.

So this week, I’m vibin’ to Money from the classic 1973 Pink Floyd album, Dark Side of the Moon. Enjoy.

💭 Quote of the Week

“The most basic question is not what is best, but who shall decide what is best”

– Thomas Sowell

📈 Charts of the Week

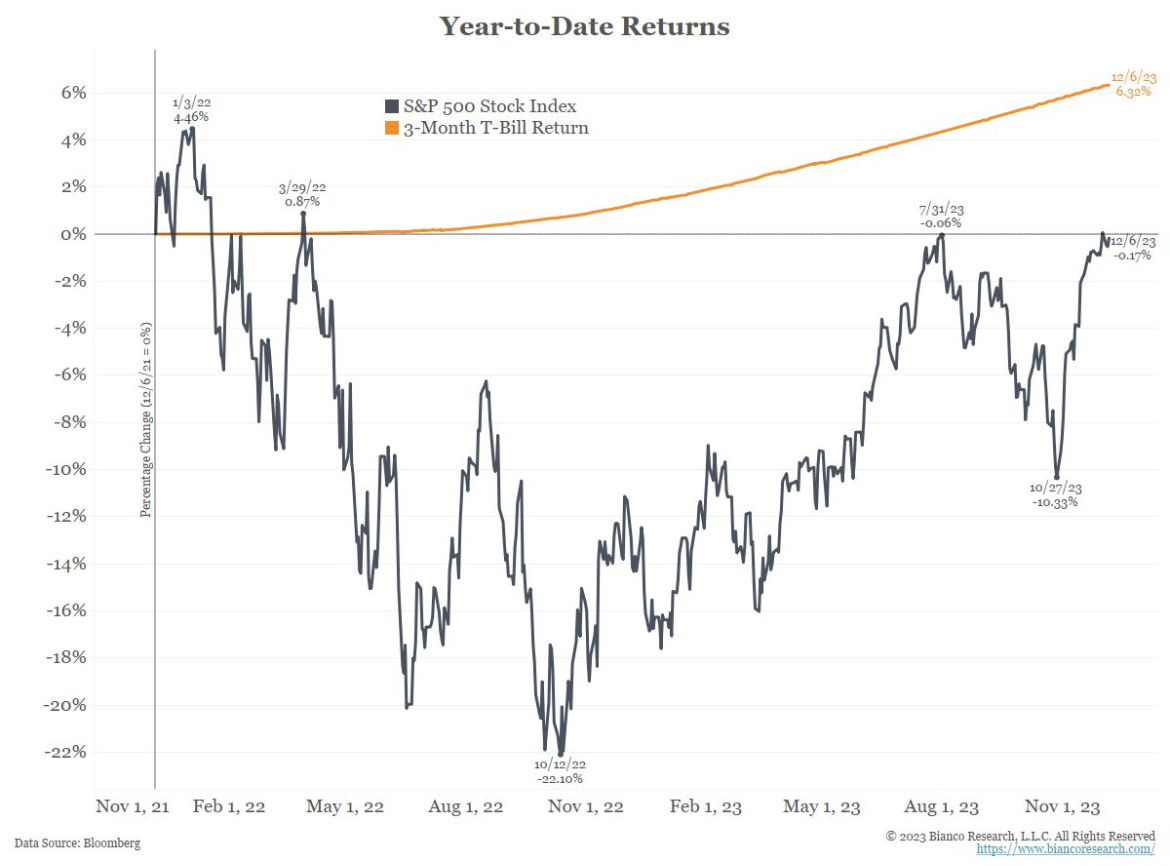

The above chart shows the rollercoaster ride to nowhere that the equity market has taken over the last two years as compared to the returns to 3 month treasuries, aka “the risk-free rate” used in the calculations by which investors determine the value of all financial assets. That’s pretty eye-opening on its own, in my opinion.

But wait. There’s more…

Reported and expected inflation continue to decline towards the Federal Reserve’s oft-stated, but entirely arbitrary goal of 2% inflation. So too have the market’s expectations for short term interest rates by mid-2024. Hey, maybe the inflation was transitory after all!

Aside from moderating inflation expectations, why else might short term interest rates be coming down next year? Well… Because they have to. 👇🏻

This third chart shows the explosion of interest payments on U.S government debt coming soon if short term rates don’t come down.

Total federal interest expenses should rise by approximately $226 billion over the next twelve months to over $1.15 trillion. For context, from the second quarter of 2010 to the end of 2021, when interest rates were near zero, the interest expense rose by $240 billion in aggregate. More stunningly, the interest expense has increased more in the last three years than in the fifty years prior.

A significant portion of the federal debt is financed using 1 to 3 year maturities, and they will need to be rolled out to future years - one way or the other. In other words, the federal government simply can’t afford to refinance its debt with short term interest rates at their current levels.

So with that in mind…

As we go into and through 2024, I continue to remain constructive on financial assets in general, particularly equities, and especially interest rate sensitive equities.

🚙 Interesting Drive-By's

This week we have articles on banking, retirement benefits, growth, and AI:

💰 On the Record with Bruce Van Saun - from Liz Hoffman at Semafor

Note: This is a great interview with Bruce Van Saun, CEO of Citizen’s Bank. He talks about the state of banking past, present, and future. Well worth the time to read. I also highly recommend Liz’s newsletter, Semafor Business.

All around Citizens Bank’s New York office, there are signs of the new reality it faces.

A TD Bank branch across the street is offering 4% interest on savings accounts. At nearby Western Alliance, six-month certificates of deposit are paying 5.7%. Even at the Wells Fargo branch in the lobby of Citizens’ offices, a three-month CD pays more than 4%.

Banks are adjusting to a world where money is no longer free. The bite is especially hard on midsized lenders like Citizens, an East Coast firm that, with $225 billion in assets, is about 1/20th the size of JPMorgan. “The cheap funding woke up,” Bruce Van Saun, Citizens’ chief executive since 2013, told me in a conversation this week.

Citizens was born out of one crisis, spun out of a bailed-out Royal Bank of Scotland in the wake of the 2008 crash. It’s now been tested by another (though Van Saun, 66, has some thoughts on the terminology) and the CEO finds himself once again picking over the industry’s wreckage for hidden gems. [link]

👀 The Pension: Rare Retirement Benefit Gets a Fresh Look - from Rethinking 65

In an economy characterized by a volatile stock market and elevated inflation, a sure thing looks better than ever. For some Americans in the labor force right now, that looks like a pension.

Striking members of the United Automobile Workers union made waves this year when the union’s leaders demanded the reopening of defined-benefit pension plans for workers hired after late 2007. Although UAW leadership failed to persuade automakers to reopen the plans, the bold move didn’t go unnoticed by retirement benefit experts.

“It was interesting that UAW did mention that in their negotiations, because that isn’t really something you would have seen 10 years ago,” said Craig Copeland, director of wealth benefits research at the Employee Benefit Research Institute, a nonprofit organization.

Only about 1 in 10 Americans working in the private sector today participates in a defined-benefit pension plan, while roughly half contribute to 401(k)-type, defined-contribution plans, which are funded with their pretax dollars and, in many cases, employer contributions.

Experts say the shortcomings of defined-contribution plans, with their assets invested by employees themselves, are more apparent in the current economic climate. [link]

🤔 IBM May Have Kicked Off a Retirement Benefit Trend - from Rethinking65

Note: A second article about defined benefit pensions, this time highlighting a forward thinking, non-unionized employer.

IBM may have just kicked off the next big trend in the world of employee retirement benefits.

Big Blue made headlines recently when it announced plans to end its 401(k) matching contribution in favor of a new benefit that walks, talks and sounds like a good old-fashioned pension. You might dimly remember them: employers contribute to the plan and manage it; when you retire, a regular check starts arriving in the mail, and it continues as long as you live.

Defined-benefit pensions are still dominant among public-sector state and municipal employers. But they have all but disappeared in the private sector as employers rushed to get them off their balance sheets over the past two decades.

IBM, often perceived as a leader in the corporate world, was one of the first large employers to announce a shift to an all-defined contribution retirement program in 2006, and the decision was a harbinger of a plunge in the number of employers offering traditional pensions.

“IBM was the huge brand name to make that move,” said John Lowell, a partner at October Three, a firm that provides consulting services to plan sponsors. “Other companies thought, ‘Well, if IBM is doing this, there must be a reason.’”

But now, IBM delivered a shock of sorts when it said last month that starting on Jan. 1, 2024, it will introduce a Retirement Benefit Account (RBA) for all of its U.S. employees. Employees can continue to contribute to their 401(k) accounts. But the match will be replaced by a contribution of 5% of pay to the RBA, along with a one-time pay increase of 1%. The pay credits will accumulate interest credits at a rate of 6% for the first three years, and will be tied to Treasury rates in the years that follow, with a floor of 3% for the first seven years. [link]

💡 Death of a Flywheel - from Evan Armstrong

Amazon and Berkshire Hathaway are in the midst of an identical, potentially fatal crisis: they are simply too successful. It’s new America, one of silicon and servers, versus old America, a nation of steel and Coke syrup.

Amazon is the fifth most valuable company in the world at roughly $1.5 trillion. Berkshire Hathaway is the eighth most valuable at $776 billion. They are also revenue giants, with Amazon pulling in $513 billion and Berkshire doing $234 billion in 2022. At this valuation and revenue size, there are very few opportunities available to meaningfully grow either business. While this is a wonderful problem to have, it is a crisis nonetheless.

The two companies pursue wholly different capital allocation strategies to combat this problem. Amazon runs hundreds of experiments at once and has flailed into all sorts of large capital expenditures, from movie studios (an $8.5 billion purchase of MGM) to internet satellites ($10B in expected capital spend) to healthcare (a $3.9 billion purchase of OneMedical). Berkshire mostly does highly concentrated buyouts or public equity purchases. Its big move this year was getting majority ownership in a gas station chain ($11 billion for a stake in Pilot).

All companies face this at some point in their existence, no matter their scale. I call it the scaled-out problem: growth plateaus for a particular business line as the marginal cost to acquire additional customers outstrips their lifetime value. Companies have to diversify their markets, their product mix, or both. If they don’t, they face a slow death by decay.

This conundrum can manifest on the scale of yeeting $10 billion dollars into satellites, or it can be as simple as a local diner expanding into Sunday brunch. By examining this problem in its most scaled, most extreme version (Amazon and Berkshire Hathaway), there are truths revealed about investing and operating that apply to everyone. [link]

⚖️ The Great AI Debate - from Peter Diamondis

The great AI debate is on... Is AI friend or foe? Is AI the road to abundance? Or the end of humanity? Are you an accelerationist (go fast!) or a doomer (slow down!)?

Do you believe AI will give us all god-like powers in the next 5 years, or overthrow humanity?

It’s hard to believe that ChatGPT is only 1 year old, and how fast it is all moving.

Question: Have you prioritized AI as *the most important tech* in your life yet? How do you view AI in your life, your company, and your industry?

Frankly, there is no more important question for you to contemplate if you’re an entrepreneur, CEO, investor, philanthropist, or business owner.

AI is so fundamental, it’s likely to have a binary outcome:

“There will be two kinds of companies at the end of this decade.

Those fully utilizing AI... and those that are out of business.”

Let’s take a quick look at some “Reasons to be concerned” vs. “Reasons to relax” about AI. [link]

👋🏼 Parting Thought

Only 15 days ‘til Christmas. 🎅

If you have any cool articles or ideas that might be interesting for future Sunday Drive-by's, please send them along or tweet 'em (“X” ‘em?) at me.

Please note that the content in The Sunday Drive is intended for informational purposes only, and is in no way intended to be financial, legal, tax, marital, or even cooking advice. Consult your own professionals as needed.

I hope you have a relaxing weekend and a great week ahead. See you next Sunday...

Your faithful financial provocateur,

-Mike